High Yield Savings Accounts Explained – A Complete Guide to Smarter Saving in 2025

Is your money sitting in a normal savings account earning very little? If your money is in a regular savings account earning only 0.01%, you are losing money every year. Maybe you are saving for a house, a car, or just trying to build an emergency fund. If your money is in the wrong place, you are missing a big chance to earn more. In 2025, every bit of money is important.

This simple guide will tell you what a High-Yield Savings Account (HYSA) is, how it works, and why now is the best time to open one. You will learn how to earn more interest and make your money grow safely.

What is a High-Yield Savings Account (HYSA)?

A High-Yield Savings Account, or HYSA, is a savings account that gives you more interest than a regular bank account. Most HYSAs are offered by online banks. These banks do not have physical buildings, so they save money on rent and staff. Because they save money, they can pay you a higher interest rate.

This builds an HYSA a smart select if you need your savings to increase faster while keeping your balance safe.

The Power of the High APY

The important difference between a regular money savings account and an HYSA is the APY, which means Annual Percentage Yield. It tells you how much money you earn in a year from interest. In 2025, most regular savings accounts pay only 0.63% interest. But many HYSAs pay between 3.5% and 5.0%, and sometimes even more.

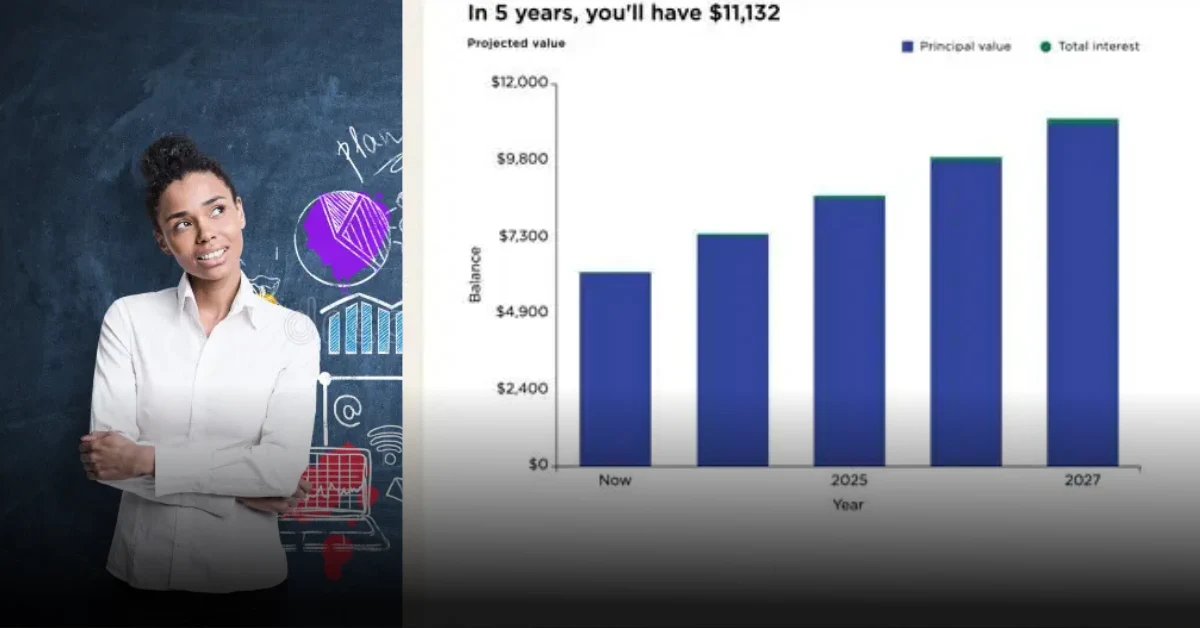

Example: If you put $10,000 in a regular account with 0.05% interest, you earn only $5 in one year. If you put that same $10,000 in an HYSA with 4.25%, you earn around $425 in one year.

That’s 85 times more money! This happens because of compound interest. That means you earn interest on your money, and then you earn more interest on that interest. Your money grows faster over time.

Safety of Funds: Are HYSAs Safe?

Yes, HYSAs are very safe. They are protected by the U.S. government, just like normal bank accounts.

FDIC Insurance Limit ($250,000)

When you open an HYSA with an FDIC-insured bank or an NCUA-insured credit union, your money is protected up to $250,000 per person, per bank. If you have a private account and a joint the account at the same bank, you can be insured for up to $500,000. Even if the bank closes, your balance is still safe.

Tip: Always make sure your online bank or app is FDIC or NCUA insured before you open an account. This is very important.

Also Read: Smart Saving Tips 2025 – Simple Ways to Manage Your Money Effectively

Usage & Goals: What Should You Use an HYSA For?

An HYSA is good for balance that you need to keep safe but still make money interest on. You can take the money out anytime, but it is correct for saving, not using.

Best uses for an HYSA:

Emergency Fund:

Save 3–6 months of living spend in your HYSA. It’s safe and make money interest while you don’t spend it.

Short-Term Goals:

Saving for a trip, a wedding, or a latest car? Keep that balance in an HYSA so it increase while you plan.

Down Payment for a Home:

If you plan to buy a house in the next few years, an HYSA is correct than the stock market because it’s safe and still payments best interest.

Holding Cash for Investing:

If you are waiting to invest later, keep your cash in an HYSA so it earns interest while you wait.

Actionable Steps: How to Open and Maximize Your HYSA

Opening an HYSA is very easy. It can take less than 15 minutes, and you can do it all online.

Step-by-Step Guide:

Compare Banks:

Look at different banks and check their interest rates. Pick one with a high APY and no fees or minimum balance rules.

Get Your Documents Ready:

You need your Social Security Number, a photo ID, and your current bank account information.

Apply Online:

Go to the bank’s website and fill out the form. Most banks make it simple and quick.

Add Money:

Move money from your main bank account to your HYSA using an online transfer.

Set Automatic Transfers:

You can set up automatic monthly transfers. This helps you save regularly and earn more with compound interest.

Also Read: How to Manage Money Wisely in 2025 – A Complete Financial Guide for Everyone

Feature Comparison

| Feature | Traditional Savings Account | High-Yield Savings Account (HYSA) |

|---|---|---|

| APY (Interest Rate) | Very low (0.01%–0.5%) | High (3.5%–5.0%+) |

| Fees & Minimums | May have fees | Usually no fees |

| Access | Limited online access | Easy online access, 24/7 |

| Best For | Everyday savings | Emergency funds, short-term goals |

The 2025 Financial Context: Why Rates are High

The strong rates in 2025 are not by opportunity. They depend on what the Federal Reserve does with interest rates. In 2024 and 2025, the Federal Reserve grows rates to control price rice. When this occur, banks also raise their savings account rates to attract latest clients.

That’s why now is a good time to open an HYSA — you can earn much more interest than before.

Interactive Quiz

Which account pays the most interest?

- Checking Account

- CD (Certificate of Deposit)

- High-Yield Savings Account

- Traditional Savings Account

Answer: 3 (High-Yield Savings Account gives the good rate and simple access)

CDs can have strong fixed rates, but your balance is locked for a right time.

Your Next Step to Smarter Saving

Now you learn how a High-Yield Savings Account duties and why it is a smart opportunities in 2025. Don’t let your balance sit in a low-interest and easy account. Transfer it to an HYSA and let it increase faster while stopping safe.

Start today — compare the best HYSAs, open one online, and enjoy watching your savings grow.

Call to Action

Share: Do you already have an HYSA? Tell us your favorite one in the comments below!

Explore: Read our next article — The Ultimate Guide to Building an Emergency Fund in a Post-Pandemic World.

Subscribe: Join our newsletter to get updates on the best HYSA rates and Federal Reserve news.

Dynamic Disclaimer

This article is for information and education only. Interest rates, APY examples, and details from 2025 may change anytime. Always check the newest rates and FDIC insurance information from your bank before opening an account.